If you farm or trade in Northern Uganda, you have almost certainly been urged to “join a SACCO.” But what is a SACCO, really, and why is it so often the answer to the access-to-finance problem that banks never solve for smallholder farmers? This guide explains what a savings and credit cooperative is, how it is governed and regulated in Uganda, and exactly how saving and borrowing work.

- A SACCO is a member-owned financial cooperative: members pool savings and borrow from the pool.

- It is owned and controlled by members on a one-member-one-vote basis, not by outside investors.

- In Uganda it is registered as a cooperative and licensed as a Tier 4 institution under UMRA / the Ministry of Finance.

- You can borrow against your savings with member guarantors, no land title needed for ordinary loans.

What a SACCO is

A SACCO, a Savings and Credit Cooperative Organisation, is a member-owned, member-run financial cooperative. Members pool their savings, and those savings become the fund that members borrow from. Most SACCOs are built around a “common bond”: members share a trade, an employer or a community. NUTOFA SACCO, for example, binds together the actors in the agricultural-mechanization value chain - tractor owners, operators, mechanics, hiring agents and farmers - across Northern Uganda.

A cooperative, in the words of the International Cooperative Alliance, is “an autonomous association of persons united voluntarily to meet their common economic, social and cultural needs through a jointly-owned and democratically-controlled enterprise.” That definition carries seven internationally recognised principles, and they are what make a SACCO different from any other lender:

Voluntary and open membership

Open to all who can use its services, without discrimination.

Democratic member control

One member, one vote, regardless of how much you have saved.

Member economic participation

Members contribute the capital and democratically control it; surplus is shared fairly.

Autonomy, education, cooperation & concern for community

The remaining principles keep the cooperative independent, train its members, work with other cooperatives, and serve its community.

SACCO vs bank: the difference that matters

A SACCO

- Owned by its members

- Board elected by members (one member, one vote)

- Not-for-profit: surplus returns to members

- Lends against savings + guarantors

- Built around a common bond and community

A commercial bank

- Owned by outside shareholders

- Board chosen by shareholders (votes by shares)

- For-profit: surplus pays shareholders

- Lends mainly against physical collateral

- Serves the general public for profit

That last contrast is the one that changes lives. A bank wants a registered land title before it lends. Most smallholder farmers don’t have one. A SACCO lends against the trust built by your savings record and the guarantees of fellow members, so finance reaches people the formal banking system leaves out.

How SACCOs are regulated in Uganda

This is worth getting right, because it is where confusion is common. Ugandan SACCOs sit under two frameworks at once:

Two ministries, two rolesA SACCO is registered as a cooperative under the Cooperative Societies Act (Cap 107) by the Registrar of Cooperatives, under the Ministry of Trade, Industry and Cooperatives. It is then licensed and supervised as a Tier 4 institution under the Tier 4 Microfinance Institutions and Money Lenders Act, 2016 (Cap 61), a function carried out by UMRA, now being absorbed into the Ministry of Finance.

A few facts that clear up the most common misunderstandings:

- What “Tier 4” means. Uganda’s financial institutions sit in four tiers. Tiers 1–3 (commercial banks, credit institutions and microfinance deposit-taking institutions) are regulated by the Bank of Uganda. Tier 4, which includes SACCOs, non-deposit-taking microfinance institutions, and money lenders, is regulated by UMRA, not the Bank of Uganda. A “Tier 4 SACCO” is simply a SACCO in this classification.

- UMRA began licensing SACCOs in 2021, and a SACCO must be licensed to conduct financial-services business. In 2024, Parliament approved folding UMRA’s functions into a new Microfinance Tier 4 Management Department within the Ministry of Finance.

- The money-lender interest cap does not apply to SACCOs. Uganda capped money lenders’ interest at 2.8% per month in 2024, but that cap explicitly does not bind SACCOs or non-deposit-taking microfinance institutions.

How saving and borrowing work

The mechanics are simple, and they are what make the model fair.

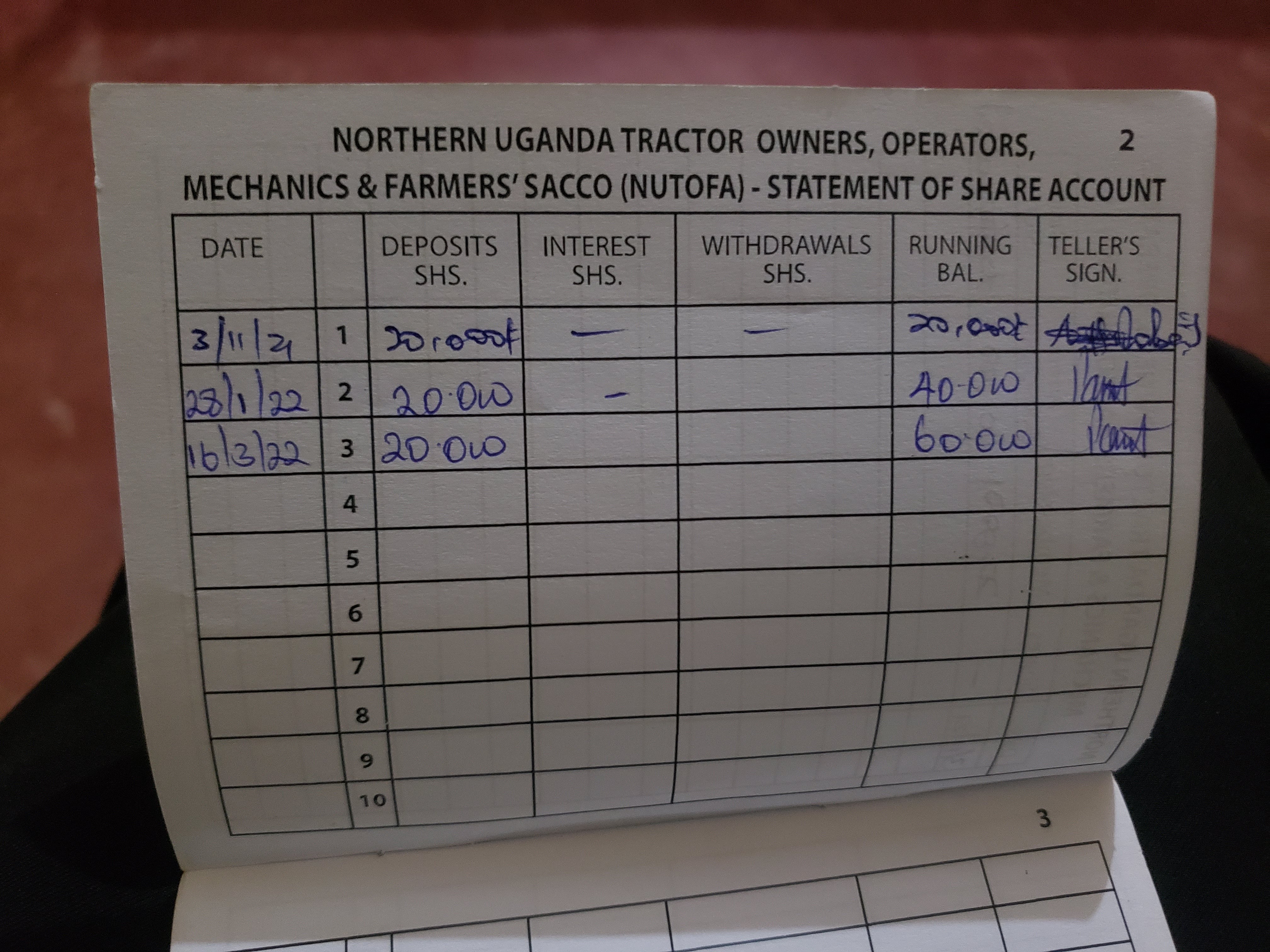

Shares vs savings

These are not the same thing, and the difference matters:

| Shares | Savings / deposits | |

|---|---|---|

| What they are | Your ownership stake in the SACCO | Money you set aside in your account |

| What they earn | Dividends, declared at the AGM | Interest on savings |

| Can you withdraw? | Not on a whim, transferable to another member on exit | Yes, on notice |

| Loan collateral? | Generally no | Yes, savings back your loan |

The save-then-borrow rule

SACCOs lend against your savings history, not your land. After a few months of consistent saving, a member can typically borrow a multiple of their standing savings, commonly up to two or three times, guaranteed by fellow members in good standing. NUTOFA, for instance, uses a three-times-savings ceiling: save UGX 500,000 and your loan ceiling is UGX 1,500,000. The exact multiple, interest and term vary by SACCO, so always ask for the specific figures.

Why this works for farmersBy substituting savings history and member guarantees for land titles, the SACCO reaches farmers no bank will serve, and because members own the SACCO, the interest you pay funds dividends that come back to members, not outside shareholders.

How to join a SACCO

Meet the common bond and basic requirements

Be 18+, of good standing, and within the SACCO's area or trade. Bring a valid national ID or passport and passport photos.

Pay the entry fee and buy shares

A one-off membership/entry fee plus a minimum share contribution. These are SACCO-specific: confirm the figures before you join.

Start saving consistently

Most SACCOs ask for a few months of regular saving before you can borrow. Your savings build both your dividend and your loan ceiling.

Apply for a loan with guarantors

Once eligible, apply through the loan committee, backed by guarantors whose savings cover your loan. Time repayment to your harvest.

SACCOs in Northern Uganda

The cooperative tradition runs deep here. Long-standing cooperative unions such as the East Acholi Cooperative Union (founded in 1969) and the West Acholi Cooperative Union have served the region for generations, and newer SACCOs have multiplied, driven partly by government channels like the Parish Development Model and Emyooga, which push funds through parish- and trade-based SACCOs. By 2023, the country had grown to tens of thousands of registered SACCOs.

NUTOFA SACCO is part of that landscape, with a specific focus: binding the agricultural-mechanization value chain into one cooperative so that members can save, borrow against those savings, and hire tractors together. Learn about our savings and loan products, how to become a member, or read about how to finance a tractor.

- International Cooperative Alliance: Statement on the Cooperative Identity (definition, values, seven principles), 1995.

- UMRA: Licensing, Regulation and Supervision of SACCOs in Uganda (Tier 4 classification; UMRA began licensing SACCOs in 2021), 2022.

- Tier 4 Microfinance Institutions and Money Lenders Act, 2016 (Cap 61); Cooperative Societies Act (Cap 107, in the 2023 revised laws).

- Parliament of Uganda: Tier 4 (Amendment) Bill 2024 absorbing UMRA into the Ministry of Finance, 2024; ICPAU/AMFIU: money-lender cap excludes SACCOs, 2024.

- The Cooperator News: Uganda's SACCOs grown to over 30,000; West/East Acholi Cooperative Unions, 2021–2023.

Frequently asked questions

-

SACCO stands for Savings and Credit Cooperative Organisation (or Society). It is a member-owned financial cooperative where members pool their savings and borrow from the common pool, usually sharing a common bond such as the same trade or community.

-

A bank is a for-profit company owned by investors. A SACCO is a not-for-profit cooperative owned by its members, who elect the board on a one-member-one-vote basis regardless of how much they have saved. A SACCO's surplus is returned to members as dividends, better savings interest or lower loan rates rather than to outside shareholders.

-

SACCOs are registered as cooperatives under the Cooperative Societies Act by the Registrar of Cooperatives (under the Ministry of Trade, Industry and Cooperatives), and licensed and supervised as Tier 4 institutions under the Tier 4 Microfinance Institutions and Money Lenders Act, 2016, a function carried out by UMRA, now being absorbed into the Ministry of Finance.

-

It depends on your savings. SACCOs lend against your savings record rather than physical collateral, commonly up to two or three times your standing savings, backed by guarantors who are fellow members in good standing. The exact multiple and terms vary by SACCO.

-

Usually not for ordinary loans. The SACCO model substitutes your savings history and member guarantors for physical collateral, which is exactly why it works for farmers who do not hold a registered land title. Larger loans may require additional security.